发布时间:2015-08-14 作者: 罗思义

None of the major advanced economies, due to general ideological opposition to State intervention in the economy, has been prepared to address the underlying problem causing slow growth - low fixed investment levels.

By John Ross

China.org.cn, August 13, 2015

China`s RMB devaluation is good news not only for China but also for the world economy. China is the main engine of global growth, therefore any weakness in its economy has negative consequences for everyone.

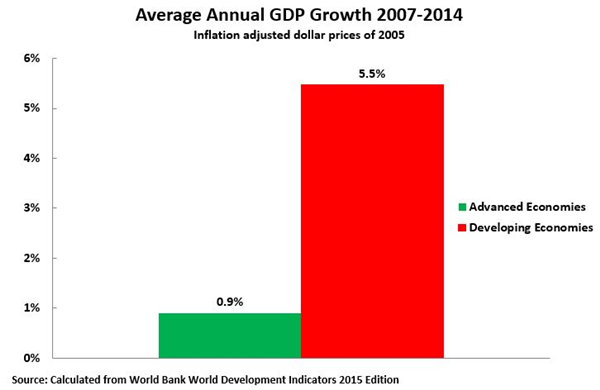

The main feature of the global economy since the international financial crisis began in 2008 has been a further deceleration in the already slow growth of the developed economies. Figure 1 shows their annual average GDP growth since 2007 has been less than 1 percent a year, compared to an average 5.5 percent for developing economies led by China. From 2007-2014 China accounted for 34 percent of world growth compared to 14 percent for the U.S., 4 percent for the EU, and 1 percent for Japan.

None of the major advanced economies, due to general ideological opposition to State intervention in the economy, has been prepared to address the underlying problem causing slow growth - low fixed investment levels. Consequently despite pressure for State infrastructure investment from leading economic figures such as former U.S. Treasury Secretary Larry Summers and Martin Wolf, chief economics commentator of the Financial Times, the advanced economies remain trapped in low growth by their dogma of "private good, State bad." Instead, they attempted to find a way out by other policies they believed were in their own interests - but which simultaneously damaged other economies and failed to overcome the underlying problem.

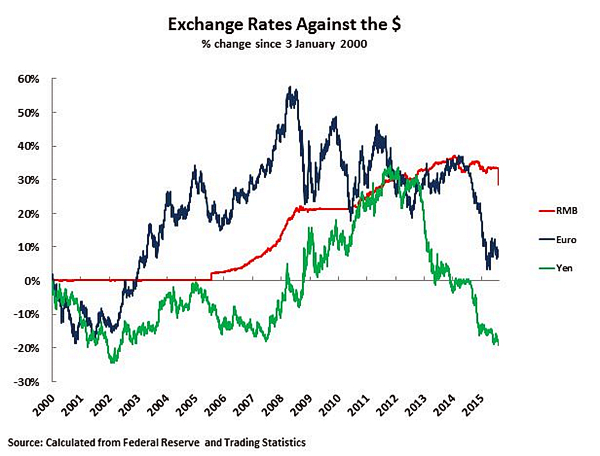

Japan`s quantitative easing (QE) under "Abenomics" created severe yen devaluation. Figure 2 shows the yen devalued against the dollar by 30 percent after Abe became prime minister in September 2012.

The Eurozone, faced with economic stagnation and Greece`s financial crisis, launched QE leading to a Euro devaluation of 26 percent since the beginning of 2014.

Japan and the Eurozone therefore both pursued policies attempting to make their exports more price competitive and imports sharply less competitive - negative policies for other countries.

The U.S. did not pursue currency devaluation - the dollar rose sharply as the yen and Euro fell. But the U.S. is increasingly concerned by a domestic asset bubble economy after years of QE and virtually zero interest rates. To try to choke these off the Federal Reserve officially indicated it would like to raise interest rates this year - despite low inflation, low wage increases and relatively slow U.S. growth.

However, as most other economies currently have low interest rates to stimulate growth, the consequences of a U.S. interest rate rise are clear - it would suck capital out of the rest of the world. Christine Lagarde, managing director of the IMF, publicly appealed for the Federal Reserve not to act this year, only to be told the Federal Reserve would be guided by U.S. domestic needs not global ones.

The advanced economies therefore remained locked in slow growth but each running internationally destabilizing policies - Japan and the EU pursuing "currency wars" and the U.S. offering the threat of a globally destabilizing interest rate rises.

The best way out of this situation would be coordinated international action. China proposed this at the G20 and in the July speech by Premier Li Keqiang to the OECD. One of China`s most well connected economists, former World Bank Vice President Justin Yifu Lin, has promoted an integrated global economic recovery plan based on China, and other capital-rich economies, financing large scale infrastructure investment in developing countries - simultaneously stimulating their growth and export markets for the sophisticated capital equipment primarily produced by developed economies. China has taken a regional initiative by creating the Asian Infrastructure Investment Bank, but the advanced economies have refused coordinated action globally.

Without this, the next best solution is for China to act by itself. Although China`s 7.0 percent GDP growth in the year is far above the others, nevertheless signs of economic slowdown have appeared. By July China`s industrial growth fell to 6.0 percent from 9.0 percent a year earlier.

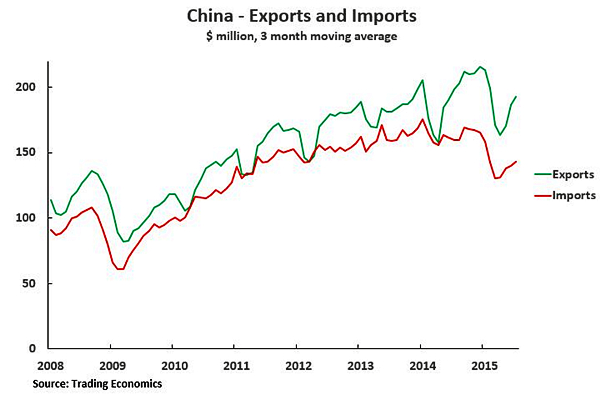

This impacts not just China but the global economy, particularly by lowering Chinese imports. By July 2015 China`s exports were down 3 percent compared to the year before but its imports had fallen 11 percent - as Figure 3 shows.

With China experiencing difficulties, the result was a dramatic fall in world commodity prices. This has extremely negative consequences for developing economies, most of which rely on commodity exports. By August 11, the day before RMB devaluation, the Bloomberg world commodity price index had fallen 27 percent compared to a year previously and by 51 percent compared to its post-international financial crisis peak.

Due to their stance against State investment, the advanced economies cannot lead a recovery of the world economy. However, China has been stimulating its economy with interest rate cuts, bank reserve requirement ratio reductions, and targeted infrastructure investment. Yet, even it could not overcome the overall 16 percent Euro devaluation, and 36 percent yen devaluation. Therefore China has now supplemented its domestic stimulus programme with a modest RMB devaluation.

For China itself evidently the consequences of measures to maintain steady growth are beneficial. But for the reasons outlined China`s position as the main engine of world growth means they are also positive for the world economy.

京公网安备 11010802037854号

京公网安备 11010802037854号