LATEST INSIGHTS

Your Present Location: LATEST INSIGHTSChina banks face huge capital hole as stimulus spurs lending

Source: Financial Times Published: 2019-3-20

Listed Chinese banks will need to raise about $260bn in fresh capital over the next three years as regulations force shadow-bank loans back on to balance sheets and global rules on systemically important groups impose extra requirements on the largest lenders.

A recent lending surge by Chinese banks in response to monetary stimulus designed to support China’s slowing economy is also adding to the banks’ capital needs, by accelerating the expansion of their balance sheets.

China’s bank regulator has forcefully implemented the global Basel III rules on bank capital adequacy as it seeks to fortify lenders against financial risks from a decade of rapid debt growth, which is now leading to record defaults.

Now, a fresh round of Chinese credit stimulus combined with new rules to curb off-balance-sheet lending have increased the pressure on Chinese banks to raise new capital.

“The government has become increasingly focused on the problem of how to channel liquidity from the banking system into the real economy,” said Bo Dikuo, president of Shanghai Chunda Asset Management. “But the constraint on bank lending from capital adequacy requirements is making financing difficult and expensive for the real economy. So there’s an urgent need for banks to replenish capital.”

Bank of China, the country’s fourth-largest lender, in January became the first Chinese bank to issue a perpetual bond — a hybrid security with a fixed coupon but no maturity date — which qualifies as additional tier one capital under the Basel rules.

The People’s Bank of China has said it will encourage commercial banks to issue perpetuals to meet capital needs, with BoC’s Rmb40bn ($5.9bn) with a 4.5 per cent coupon seen as a benchmark. Previously, Chinese banks relied on preference shares, sometimes known as contingent convertible (CoCo) bonds, to meet the additional tier one requirement.

“The demand for BoC’s perpetual was pretty OK,” said an investment manager at a Chinese asset management group in Hong Kong. “Current onshore yields are so low that everyone is chasing yield. These capital instruments still offer certain pick-up versus the banks’ senior notes.”

But additional tier one and tier two capital represent less than a tenth of Chinese banks’ overall capital needs. Listed banks will need to raise Rmb1.74tn in regulatory capital over the next three years, excluding the amount they are expected to generate internally through retained earnings, according to an estimate by Central China Securities.

Of this total, about Rmb1.6tn must be core tier one capital. For that category, only common equity qualifies.

Many banks have relied on private placements to major shareholders to raise equity. Convertible bonds are also an attractive solution because they offer a way around a Chinese rule forbidding state-owned enterprises from selling shares below book value. Bank shares have frequently traded below that level in recent years, restricting their ability to issue new shares.

“There are some new capital instruments such as perpetual bonds, and regulators are also lowering the obstacles for some instruments that were already in use — such as convertibles and preferred shares — so that more banks can use them,” said Dong Ximiao, senior researcher at Renmin University’s Chongyang Institute for Financial Studies in Beijing.

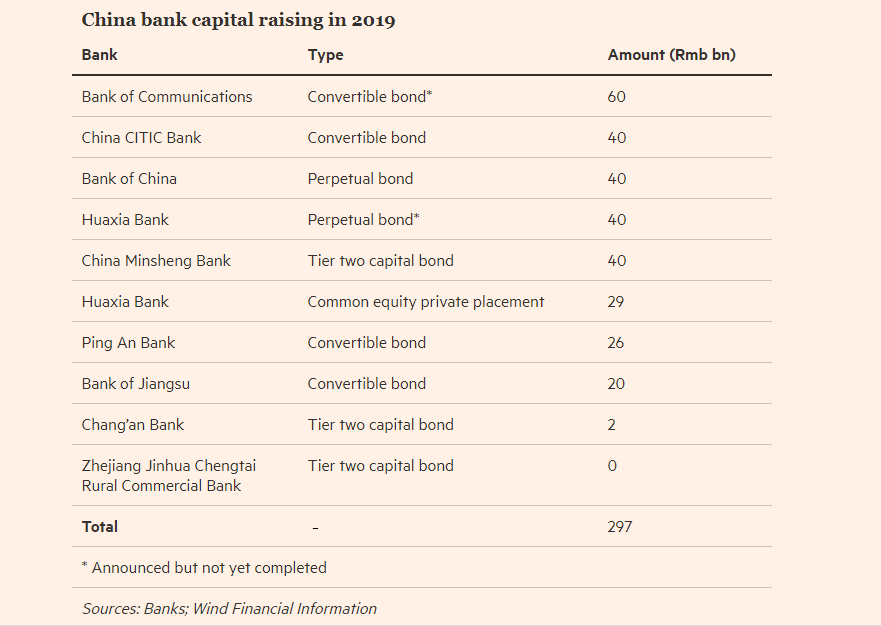

Since the start of 2019, nine commercial banks have issued or announced plans to issue capital securities totalling up to Rmb297bn, according to data from Wind Financial Information. The securities include common shares, convertible bonds, and subordinate bonds that qualify as tier two capital under the Basel rules.

Beyond Basel III, the largest Chinese lenders also face additional requirements to for so-called “total loss-absorbing capacity”, a category of liabilities similar to regulatory capital. This requirement applies to lenders that the Financial Stability Board, an arm of the G20, has designated as globally systemically important banks.

For emerging markets, including China, such banks will have to meet total loss-absorbing capacity requirements beginning in 2025, with a higher requirement taking effect in 2028. Moody’s estimates that the four biggest Chinese commercial banks — Industrial and Commercial Bank of China, China Construction Bank, Agricultural Bank of China, and BoC — will need to raise a further Rmb2.8tn in capital to meet this requirement.

Finally, Chinese regulators led by the People’s Bank of China said last year that they will take inspiration from the global framework and designate some lenders as domestic systemically important banks, thereby subjecting them to additional capital requirements.

The banking regulator has set the minimum capital adequacy ratio for domestic systemically important banks at 11.5 per cent of risk-weighted assets, compared to the normal 10.5 per cent requirement.

Some experts believe that regulators will also announce an additional capital buffer requirement when they publish the initial list of domestic banks later this year. That could increase these banks’ capital needs by tens of billions of dollars.

“At this point we still don’t if there’s going to be an additional buffer if and when they disclose the list of domestic banks,” said Grace Wu, senior director of financial institutions at Fitch Ratings, adding uncertainty to how much new capital the banks will ultimately require.

Dong Ximiao is associate dean of Chongyang Institute for Financial Studies at Renmin University of China.

Key Words: China; bank; capital hole; Dong Ximiao

京公网安备 11010802037854号

京公网安备 11010802037854号